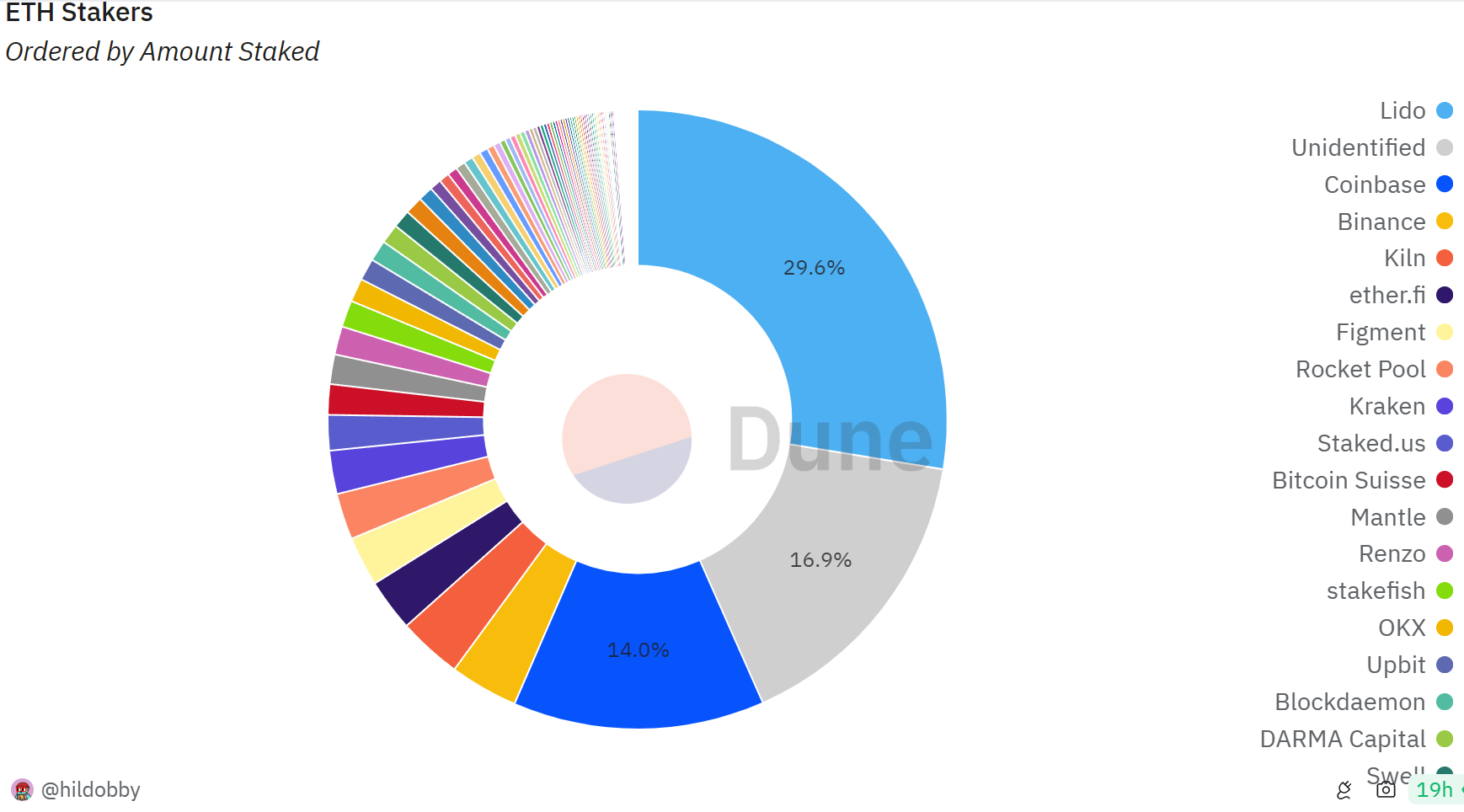

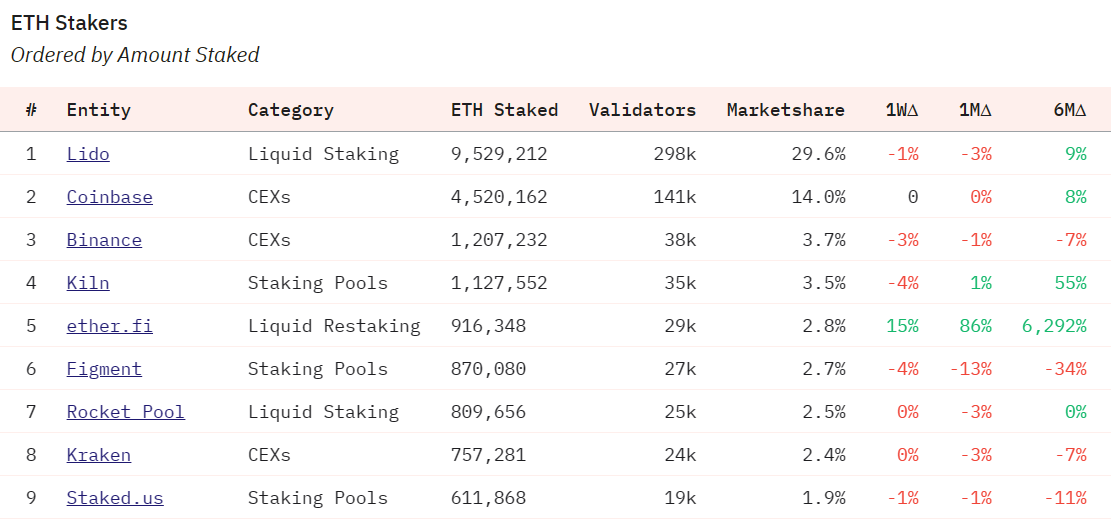

The recent surge in Ethereum stakers has led to a decrease in the market share of Lido, a liquid staking solution, from 32% in December 2023 to 29.57%. This decline has alleviated concerns about Lido’s dominance in the ecosystem.

Lido’s popularity in Ethereum staking, combined with a lack of competition, had allowed it to capture the majority of the ETH staking market. However, there were worries within the community about any single entity having over 33% control, potentially influencing Ethereum’s blockchain.

As of April 4, data from Dune, a crypto analytics platform, indicates that Lido’s market share for staked ETH has fallen below 30%. Other significant contributors to the ETH staking ecosystem include Coinbase (14.04%), Binance (3.75%), and Kiln (3.5%).

However, the second-largest entity in ETH staking is labeled as “unidentified,” representing 16.9% of the market.

In total, there are 26 known entities contributing to ETH staking, including crypto exchanges like Kraken (2.4%), Bitcoin Suisse (1.6%), OKX (1.2%), and Upbit (1.1%).

According to Ethereum co-founder Vitalik Buterin, stake pools should not exceed 15% control and should adjust their fee rates accordingly to maintain decentralization.

Speculative controversial take: we should legitimize price gouging by top stake pool providers. Like, if a stake pool controls > 15%, it should be accepted and even *expected* for the pool to keep increasing its fee rate until it goes back below 15%. https://t.co/cOtuM7Occd

— vitalik.eth (@VitalikButerin) May 14, 2022

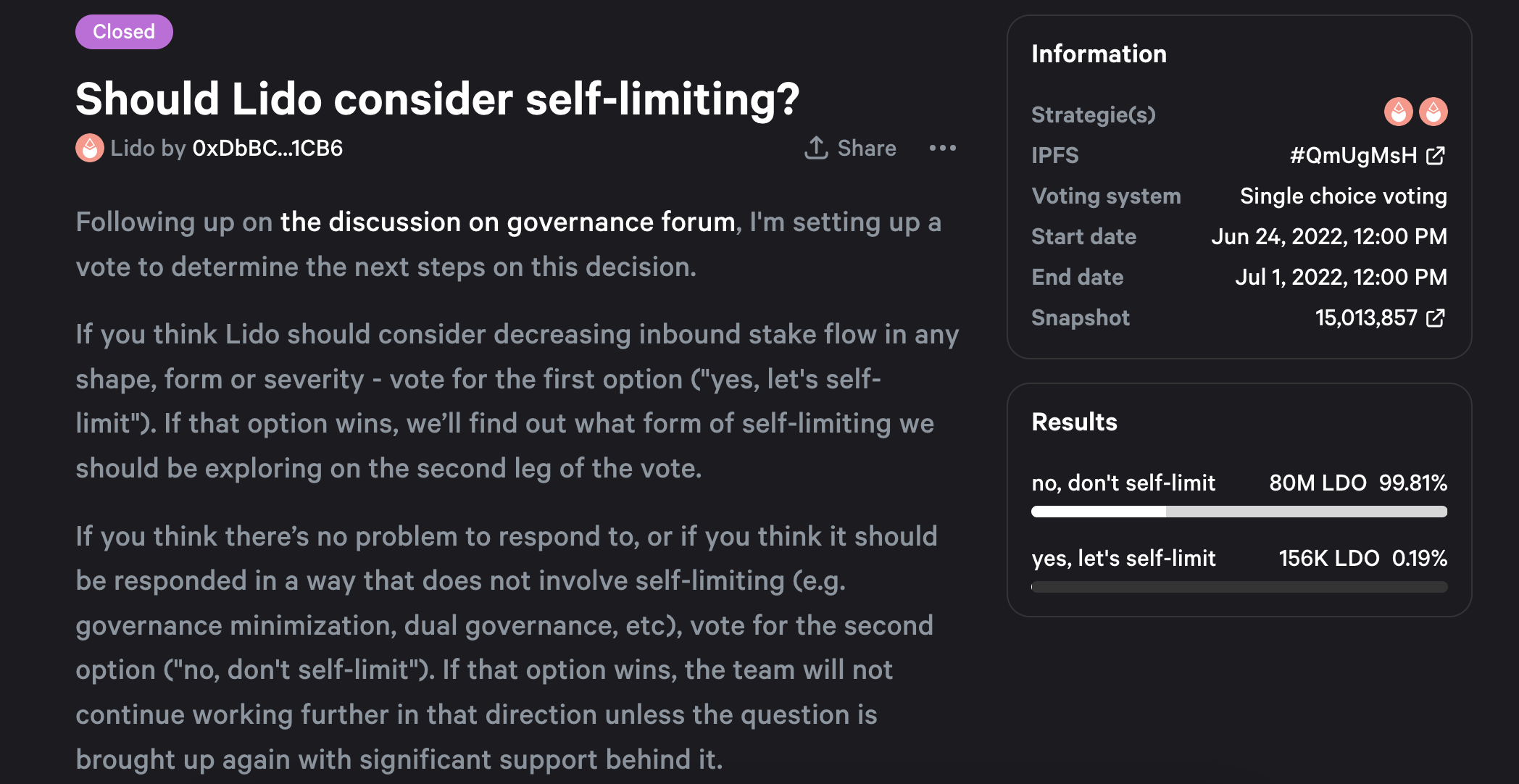

Previously, the Lido decentralized autonomous organization (DAO) community attempted to address the dominance issue by proposing a hard limit in May 2022. However, the proposal was rejected by the DAO with a 99.81% vote in June 2022.

Increasing competition among ETH staking service providers is expected to contribute to further decentralization in the staking ecosystem.

In a recent Coinbase report, analysts highlighted risks associated with ETH restaking and the issuance of liquid restaking tokens (LRTs). They pointed out that while restaking can increase earnings, it also compounds risks by allocating funds to similar validators for higher yields. This could lead to a higher, albeit hidden, risk profile for LRTs.